|

|

|

|

|

|

|

|

|

|||

|

|

|

|||||||

|

|||||||

|

|||||||

|

|||||||

|

|||||||

|

|||||||

|

||||||

|

||||||

|

||||||

|

||||||

|

|

|

|

|

|

|

|

auto warranty providers, a quick tradeoff guide for efficient buyersYou want fewer surprises and faster approvals, not brochures. That's the point of evaluating providers: turn a potential four-figure repair into a predictable, controllable cost - without sacrificing repair quality or time. What they actually doThese contracts cover certain repair costs after the factory warranty ends. A provider (often the administrator) handles claims, the obligor carries legal responsibility to pay, and sometimes an insurer backs the risk. Reliable setups make this chain visible and simple. Core functions

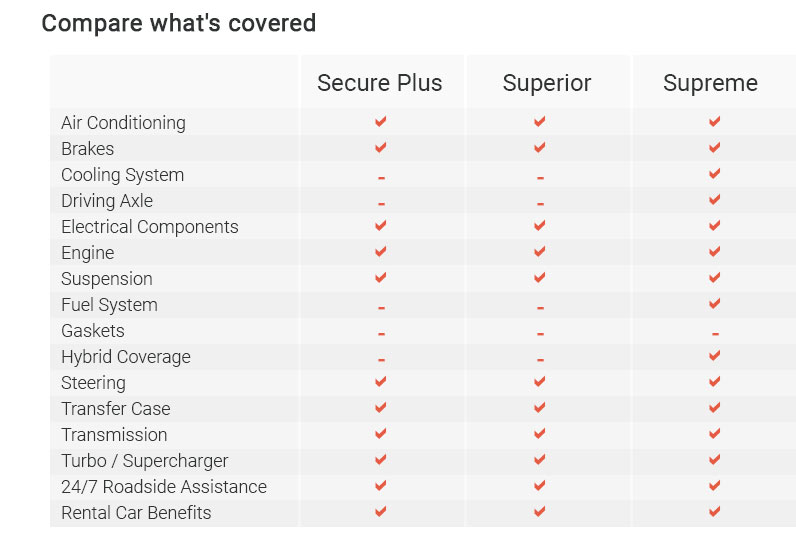

Coverage tiers decodedNames vary; the mechanics don't.

Tradeoffs that matter

Cost math, quickTypical multi-year plans range widely. Focus on expected repairs: one A/C system overhaul or timing component job can rival the contract price. If your vehicle's known weak spots exceed the premium + deductible + likely exclusions, the math leans yes; otherwise, keep a repair fund. Reliability signals

One-minute claim drill (real-world)Alternator dies on a rainy Thursday evening; I call from a rest stop, get a claim number in minutes, tow to a shop that opens at 7 a.m., and the advisor phones the provider with the diagnosis. Authorization lands before lunch; rental is covered to the daily cap. That's the experience you want - predictable and quick. Red flags

Who usually benefits

How to compare in 20 minutes

Minor backtrack: pricing nuanceI said cheaper monthly isn't always cheaper. More precisely, refundable plans with pro-rata cancellation and no finance charges can beat a lower monthly price that's heavily marked up with dealer financing. Always total the lifetime cost. If you use a dealerDealers can add margin in the finance office. Ask for the cash price, the administrator's name, and time to read the contract. You can often negotiate or buy later before factory coverage ends. Quick glossary

Bottom lineEfficient picks share three traits: transparent contracts, fast authorizations, and credible financial backing. If a provider can't demonstrate those quickly, skip it and keep your repair fund ready. https://www.top10autowarranties.com/extended-auto-warranty-state/north-carolina

We compared all the top rated providers and have generated a list of our Top 10 Extended Car Warranty Providers in North Carolina. https://www.totalautoprotect.com/state/north-carolina

Extend The Life Of Your Vehicle! Total Auto Protect offers peace of mind. A standard manufacturer warranty lasts just a few years until your automobile actually ... https://www.nationwideautowarranty.com/

NationWide Auto Warranty is one of Canada's largest automotive warranty providers. Based out of Waterloo Ontario, our experienced staff have been providing ...

|